Institutional Insights: BNPP 'SpaceX - How To Trade It'

The key message is that the expected SpaceX IPO is being framed less as a simple single-name listing and more as a major market-liquidity event. If it becomes the largest IPO ever, the deal will not only attract enormous retail, institutional, thematic, and passive attention, but it will also test the market’s ability to absorb a very large new equity supply event at a time when positioning, volatility, and index-flow mechanics are already important drivers of price action.

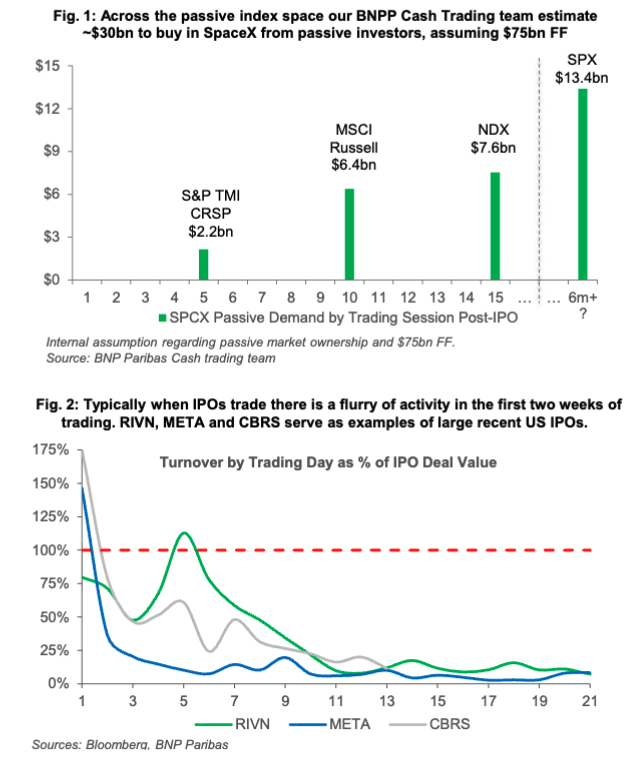

The most important point is that SpaceX would be a call on liquidity. In normal conditions, a large IPO can be absorbed if risk appetite is strong, cash balances are available, and investors are willing to rotate capital. But a record-sized IPO creates a more complex flow problem: buyers need to source cash, funds may need to rebalance, passive products may eventually need to prepare for index inclusion, and investors may sell existing winners to make room. That means the SpaceX IPO could trigger meaningful selling elsewhere even if demand for SpaceX itself is extremely strong.

The timing matters because US retail wealth effects are currently very strong, helped by recent gains in semiconductors and AI-linked equities. Retail investors have more embedded gains, more confidence, and more willingness to participate in high-profile growth stories. SpaceX is uniquely suited to capture that attention because it combines space, defense, satellites, communications infrastructure, Elon Musk, and a quasi-AI/strategic-tech narrative. From a demand perspective, that is powerful. But from a market-structure perspective, it also means demand could be crowded, emotional, and highly procyclical.

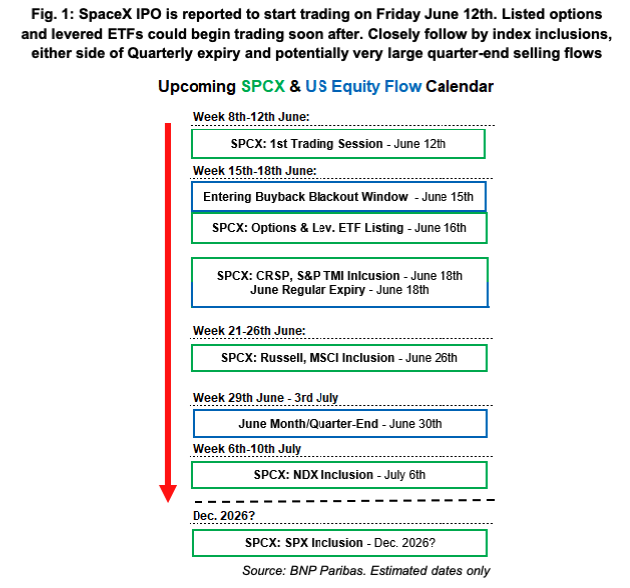

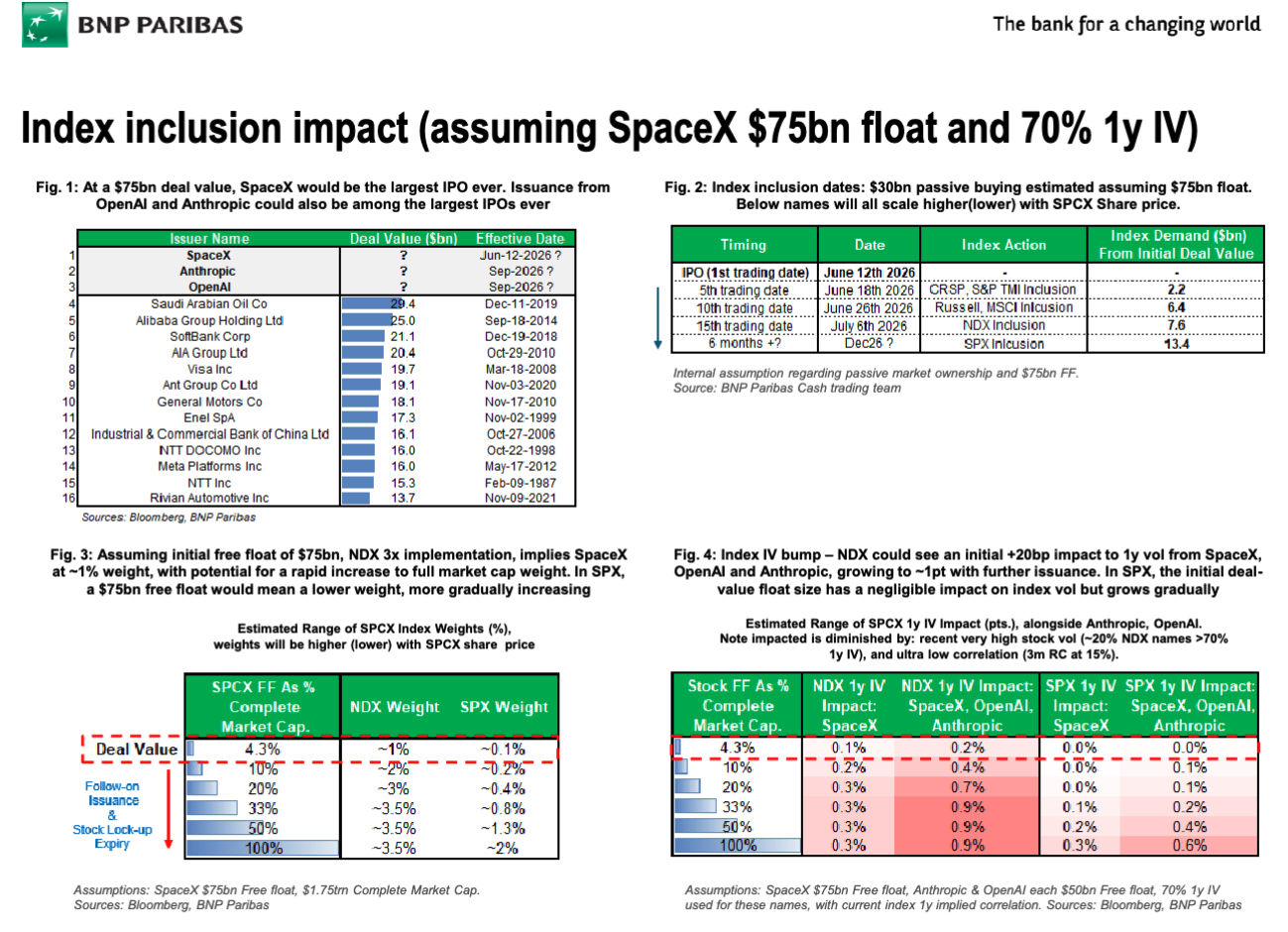

The index-rule-change angle is also critical. Headlines around possible large passive buying flows can create anticipatory demand for SpaceX, but passive buying into one large new constituent mathematically implies selling elsewhere. That selling can create a short-gamma-like effect around SpaceX’s share price. If SpaceX rallies, passive and benchmark-sensitive investors may need to buy more SpaceX and sell more of other holdings to fund it. If SpaceX falls, the flows can reverse or create pressure through deleveraging and risk-control mechanisms. The larger the stock’s market cap, the larger the potential rebalance impact.

IPOs already tend to have high volatility and fat tails, especially when the company is highly visible, difficult to value, and subject to retail and institutional demand surges. SpaceX would likely check all of those boxes. The difference this time is scale. A normal volatile IPO can create large single-name moves without necessarily affecting the index. A SpaceX IPO, if it launches at an unprecedented market cap, could combine IPO-level volatility with mega-cap-level market weight. That makes it potentially systemic from a flow and volatility perspective, even if the company-specific fundamentals remain attractive.

The note’s central concern is not that any one SpaceX-related flow is unmanageable. Standalone demand from retail, institutions, ETFs, benchmark funds, or thematic investors might each be digestible in isolation. The problem is that many of the flows could be same-way and additive. Retail FOMO, institutional allocations, passive anticipation, benchmark pre-positioning, thematic ETF demand, hedge-fund momentum chasing, and selling of existing Tech/Semi winners could all occur at roughly the same time. When many investors need to do the same thing at once, liquidity can deteriorate quickly.

This is why the note highlights the risk of higher market volatility over the next month. The equity market is already dealing with several other flow-heavy events: megacap issuance, AI infrastructure capital raises, elevated ECM activity, month-end/quarter-end rebalancing, NFP, Middle East risk, tariffs, and large rotations between momentum and laggards. Adding the largest IPO ever into that environment could amplify existing fragility. The danger is not the base case; the danger is that forced buying and forced selling interact with thin liquidity and crowded positioning.

Forced flows and illiquidity are often present in the fattest market tails. That is the main risk-management message. When investors are forced to buy SpaceX because of benchmark, passive, or momentum pressure, and simultaneously forced to sell other equities to fund that purchase, the market can experience unexpected volatility even if the macro backdrop is not deteriorating. Similarly, if SpaceX trades poorly after listing, the failure of a marquee IPO could damage sentiment, pressure related high-growth assets, and create de-risking in areas that had been used as funding sources.

The current volatility setup makes this risk more asymmetric. VIX and VVIX are at year-to-date lows, meaning broad index volatility and vol-of-vol are relatively cheap. SMH put skew is also at lows, meaning downside protection in semiconductors is relatively inexpensive versus recent history. That matters because semiconductors are likely one of the natural funding sources for SpaceX demand, given their strong recent gains and the retail wealth effect created by the sector. If investors sell Semi winners to buy SpaceX, SMH could be vulnerable, especially if the broader AI trade is already crowded.

The hedge opportunity is therefore not necessarily about predicting that the SpaceX IPO will go badly. The note explicitly frames hedging as protection against the tails of what might happen, not the base case. The base case may be that the IPO is successful, demand is strong, and the market absorbs it. But the tail risk is that the IPO creates a liquidity vacuum, forced selling in existing winners, violent rotations, and higher index volatility. In that scenario, owning cheap index vol, vol-of-vol, or Semi downside convexity could be attractive.

From a trading perspective, the most exposed areas are likely the biggest funding sources: semiconductors, megacap Tech, AI infrastructure winners, momentum, and other high-profit pools where investors have gains to monetize. SMH put skew being low is relevant because Semi downside hedges may offer relatively efficient protection against a funding unwind. Nasdaq and high-momentum baskets could also be vulnerable if investors rotate capital from crowded AI winners into SpaceX. Conversely, if SpaceX demand is funded by broad equity selling, S&P volatility could rise even if the IPO itself trades well.

The SpaceX IPO could also affect breadth in two different ways. In one scenario, it supports risk appetite by validating deep liquidity, retail enthusiasm, and demand for frontier growth assets. That would likely be bullish for high-beta growth, thematic tech, and speculative innovation. In another scenario, it drains liquidity from the rest of the market, causing selling pressure in prior winners and making the index more fragile. The distinction depends on whether the IPO brings in fresh capital or forces rotation from existing equity holdings.

The practical takeaway is to view SpaceX as a liquidity stress test. A successful deal with orderly secondary-market trading would confirm that risk appetite remains deep and that the market can absorb record issuance. But disorderly trading, excessive passive-flow anticipation, or obvious funding pressure in Semis/Tech would be a warning sign that the market’s surface calm is masking liquidity fragility. With implied volatility low, the market is not paying much for these tails.

The SpaceX IPO may be the summer’s most important catalyst because of its size, visibility, retail appeal, and potential passive-flow consequences. The fundamental story may be exciting, and many flows may be digestible individually, but the combination of same-way buying in SpaceX and same-way selling elsewhere could create market-wide volatility. With VIX, VVIX, and SMH put skew near lows, hedging looks attractive not because a bad outcome is the base case, but because the market appears underpriced for the liquidity tails a record IPO could generate.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!