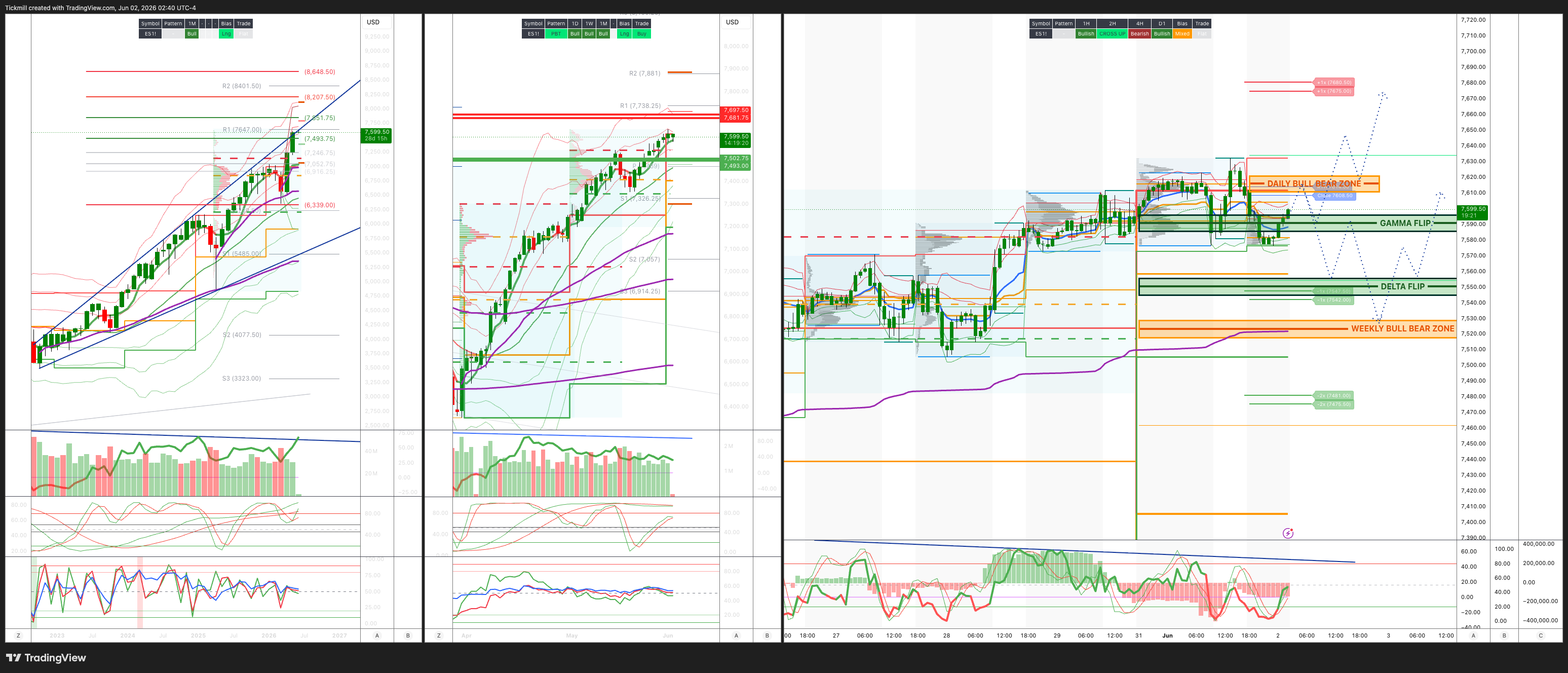

S&P500 Daily Action Areas & Price Targets 2/6/26

S&P500 Daily Action Areas & Price Targets 2/6/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7535/25

WEEKLY RANGE RES 7680 SUP 7500

June MOPEX Straddle: 274pt range implies a OPEX to OPEX range of [7134, 7683]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.06 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BULLISH 7585

WEEKLY VWAP BULLISH 7480

MONTHLY VWAP BULLISH 7036

DAILY STRUCTURE - OTFH 7576

WEEKLY STRUCTURE – OTFH - 7515

MONTHLY STRUCTURE - OTFH - 7199

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFL): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7585/75

GAMMA FLIP 7590

DELTA FLIP 7550

DAILY RANGE RES 7680 SUP 7447

2 SIGMA RES 7741 SUP 7480

VIX BULL BEAR ZONE 19

TRADES & TARGETS

SHORT ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET DAILY RANGE SUP

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Under The Hood’

US equities were mixed to start the week, with the Nasdaq again leading while small caps lagged. The S&P 500 rose 26bps to 7,560 despite a $3.05bn MOC sell imbalance, the Nasdaq 100 gained 60bps to 30,514, the Russell 2000 fell 46bps to 2,906, and the Dow added 9bps to 51,079. Volumes were very heavy at 21.8bn shares across US exchanges versus a YTD daily average of 19.1bn, consistent with the post-month-end, high-dispersion, high-factor-volatility environment. Cross-asset, the latest cautious Middle East headlines pushed oil sharply higher, with WTI up 571bps to $92.35, while the 10-year yield rose 2bps to 4.45%. VIX rose 478bps to 16.05 even as the S&P finished higher, reinforcing the recent positive spot/vol correlation. Gold fell 126bps to 4,484, DXY rose 24bps to 99.18, and Bitcoin remained weak, down 291bps to 71,490.

The headline index move again understated the amount of frustration and dispersion under the surface. The dominant topic was software, which has now outperformed the S&P 500 by more than 10 percentage points over two sessions, by far the largest two-day stretch of outperformance in more than 25 years. This move is being treated less as a clean fundamental re-rating and more as a flow, positioning, and optionality event. The desk has seen some inflows, but stocks are moving much faster than positioning and sentiment have adjusted. That matters because it means the squeeze can continue if investors are still underweight, but it also means the move is vulnerable to reversal if flows slow or if upcoming catalysts fail to validate the narrative.

Most investors remain reluctant to attach a strong incremental fundamental explanation to the move in SaaS and applications software. There is more open-mindedness around security and data infrastructure, where the AI adjacency and earnings evidence feel more credible after recent prints from SNOW, OKTA, MDB, and related names. But for the broader SaaS/apps universe, the rally appears to be driven more by the violent unwind of underweights, crowded shorts, and call-option demand than by a sudden change in bottom-up fundamentals. That distinction is important. Software may now be the key broadening test for the market, but the quality of the move varies meaningfully by subsector.

Options activity underscores how flow-driven the software move has become. Total call-option volume on IGV posted its biggest day ever on Friday, with 280k contracts traded, followed by another 225k contracts today. Inbounds have focused much more on flows and the expected duration of the move than on single-stock selection. That is classic squeeze behavior. Investors are trying to determine how long the chase can last rather than debating which individual software companies deserve higher earnings estimates. With Microsoft Build, Snowflake Summit, Cisco Live, Computex, and other AI-related events this week, the market has enough catalysts to keep the trade alive, but expectations are rising quickly.

Consumer focus at the start of the week was centered on housing after Berkshire agreed to buy TMHC for roughly $7bn in cash, sending TMHC up 22%. The deal is notable as the first major purchase under incoming chief executive Greg Abel and reads as a vote of confidence in the US housing market. That aligns with the prior observation that long-term buyers have been increasingly interested in housing-related consumer names despite broader consumer caution. Elsewhere, YUM was said to be in exclusive talks to sell Pizza Hut to LongRange Capital, following the strategic review originally announced in November 2025. MGM rose 16% and IAC gained 1% on reports that Barry Diller’s People Inc is preparing a $48.30/share offer for MGM Resorts, a roughly 10% premium to Friday’s close. Taken together, consumer M&A is helping offset some of the skepticism around near-term spending trends.

Floor activity was moderate at a 5 out of 10, but the desk finished meaningfully skewed to buy, at +465bps versus a 30-day average of +70bps. Single-stock flows were muted to start the week, with both asset managers and hedge funds finishing as slight net buyers. Buying was driven by macro products and tech, partially offset by supply in communication services and utilities. This fits the Prime Brokerage theme from last week: hedge funds are adding market-level beta and tech exposure, but single-name conviction is more mixed as dispersion remains extreme.

The derivatives picture remains important because the market continues to show positive spot/vol correlation. Equities can rally while volatility also rises, particularly when headlines are driving fast rotations and investors are chasing upside while still wanting protection. S&P average single-stock one-month put-call skew is now at the lowest level in the 24-year dataset, meaning downside puts are extremely cheap versus calls at the single-stock level. The vol panic index has fallen near two-year lows at 1.38 out of 10, led by Friday’s vol crush and the decline in the term structure. Despite fresh geopolitical headlines during the session, the desk saw little demand for hedging, which suggests investors are not yet treating the Middle East updates as a reason to de-risk aggressively.

Flow-wise in options, clients have been buying volatility in the S&P while selling volatility in QQQs. That makes sense given the setup: index-level geopolitical and macro risk is still relevant, while Nasdaq and software upside has become heavily demanded and perhaps more expensive. Clients have also been buying upside in software and MSFT into the Build catalyst this week. The desk likes selling IWM three-month volatility as the market moves closer to the Russell rebalance at the end of June, likely reflecting the view that small-cap implied vol remains rich relative to likely realized outcomes, especially with RUT still lagging and not participating as cleanly in the current software/AI squeeze.

The straddle for the rest of the macro-heavy week is 1.02%. With the S&P closing at 7,560, that implies roughly a 77-point move through the remaining events and an approximate range of 7,483 to 7,637. This is slightly below the earlier full-week implied move of 1.2%, but still meaningful given the upcoming JOLTS, ISM Services, and nonfarm payrolls. If the S&P stays inside that range, the market can likely remain in a rotation-friendly regime, with software, AI-adjacent laggards, fintech, and select housing/consumer names continuing to work. A break above the top of the range would likely force more upside chase, especially given the amount of software call buying and short-covering dynamics. A break below the lower end would likely refocus investors on the fragility of a flow-driven software move, the rebound in oil, and the risk that rates and geopolitics begin to matter again.

The index tape remains constructive but increasingly strange. Oil is back above $92, VIX is rising with spot, small caps are lagging, and yet Nasdaq and software continue to squeeze higher. That is not a calm broad-based rally; it is a market dominated by factor volatility, positioning gaps, and catalyst chasing. The software move is historically extreme and may have further to run if underweights are forced to cover, but the fundamental bar is rising quickly. In this environment, the better stance is to respect the squeeze, lean into higher-quality data infrastructure/security and AI-adjacent software over broad SaaS beta, and use the unusually cheap put skew to add selective downside protection as the macro calendar unfolds.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!