Institutional Insights: Goldman Sachs "Vol Colour - The Set Up'

Bottom line: While historical patterns suggest geopolitical volatility tends to subside relatively quickly, the current environment remains exceptionally challenging. We are facing intersecting concerns—ongoing issues with AI, private credit, and now heightened geopolitical tensions. Compounding these challenges, the technical setup is increasingly precarious. Dealers are short gamma, implied volatility is elevated, liquidity is constrained, and positioning remains high.

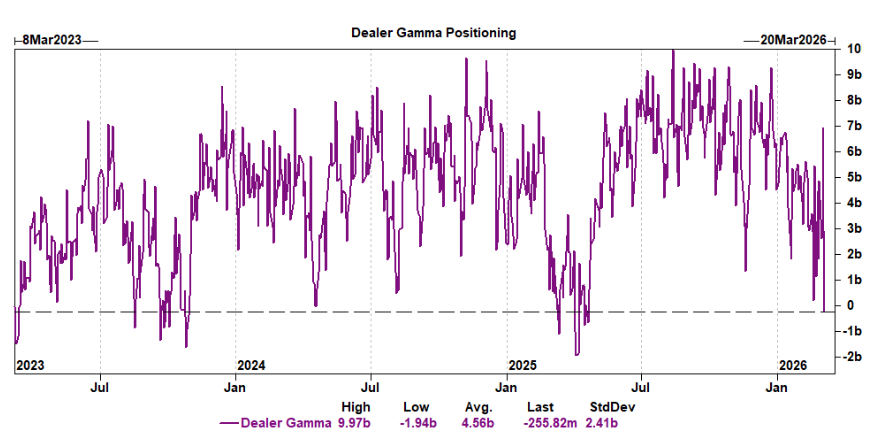

Dealer gamma (via SqueezeMetrics) dropped sharply last week, turning negative for the first time since April 2025. We estimate that the ~6500 level represents a significant short gamma zone, meaning downward moves could be amplified, all else being equal. Signs of strain appeared in the volatility market on Friday as the session closed. The front-month VIX future ended near 27, outperforming its beta to SPX by nearly 3 points. Meanwhile, the VVIX Index (volatility of VIX) closed above 140.

Across indices, front-month implied volatility is trading in the 20s—the highest levels since April 2025—while skew remains persistently steep. Our US Vol Panic Index is now at 9.72 out of 10, signaling extreme hedging difficulty. In this environment, we favor strategies that involve net selling of volatility, such as ratio put spreads or put spread collars.

Liquidity conditions have worsened. On Friday, the top-of-book depth for the S&P was just $5 million, while VIX liquidity averaged only 108 contracts on the touch—ranking in the 13th and 9th percentiles over the past year, respectively. From a prime brokerage perspective, US equities were net sold for a third consecutive week (-0.2 standard deviations versus the past year), primarily driven by outflows from macro products. Interestingly, single stocks were net bought for the first time in five weeks (+1.2 standard deviations), leading to a slight decrease in overall gross exposure but a surprising increase in fundamental long/short gross exposure. With uncertainty at these levels and hedges proving difficult to secure, the market appears to be shifting toward de-grossing, though this trend has yet to fully materialize.

Similarly, systematic strategies have not yet meaningfully reduced risk. CTAs remain long $36 billion in US equities. As of Friday, we closed below the medium-term threshold (~6760), signaling that sell estimates will start to rise. If volatility persists, this segment of the market will likely attract increased attention.

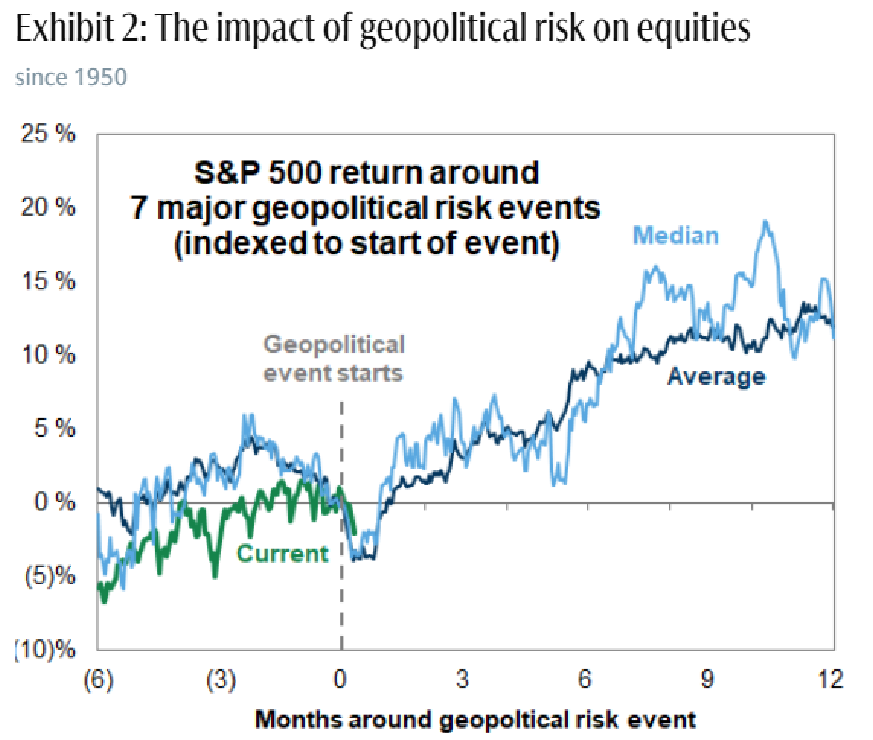

Zooming out, the market's reaction to the current geopolitical shocks aligns with historical precedents. During seven spikes in the Geopolitical Risk Index since 1950, the S&P 500 declined by an average of 4% during the first week. Historically, equities have typically rebounded to pre-shock levels within a month, though outcomes have varied widely.

That said, there are no indications that volatility will ease in the near term. As of Friday’s close, the options market is pricing in a 2.86% move for the S&P 500 in the coming week.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!